Table of Content

- Minimum Credit Score to Buy a House

- How much more will it cost to buy a house with bad credit?

- Thinking about buying but not sure where to begin? Start with our affordability calculator.

- Mortgage Rates by State

- Next: Discuss your options with a local lender.

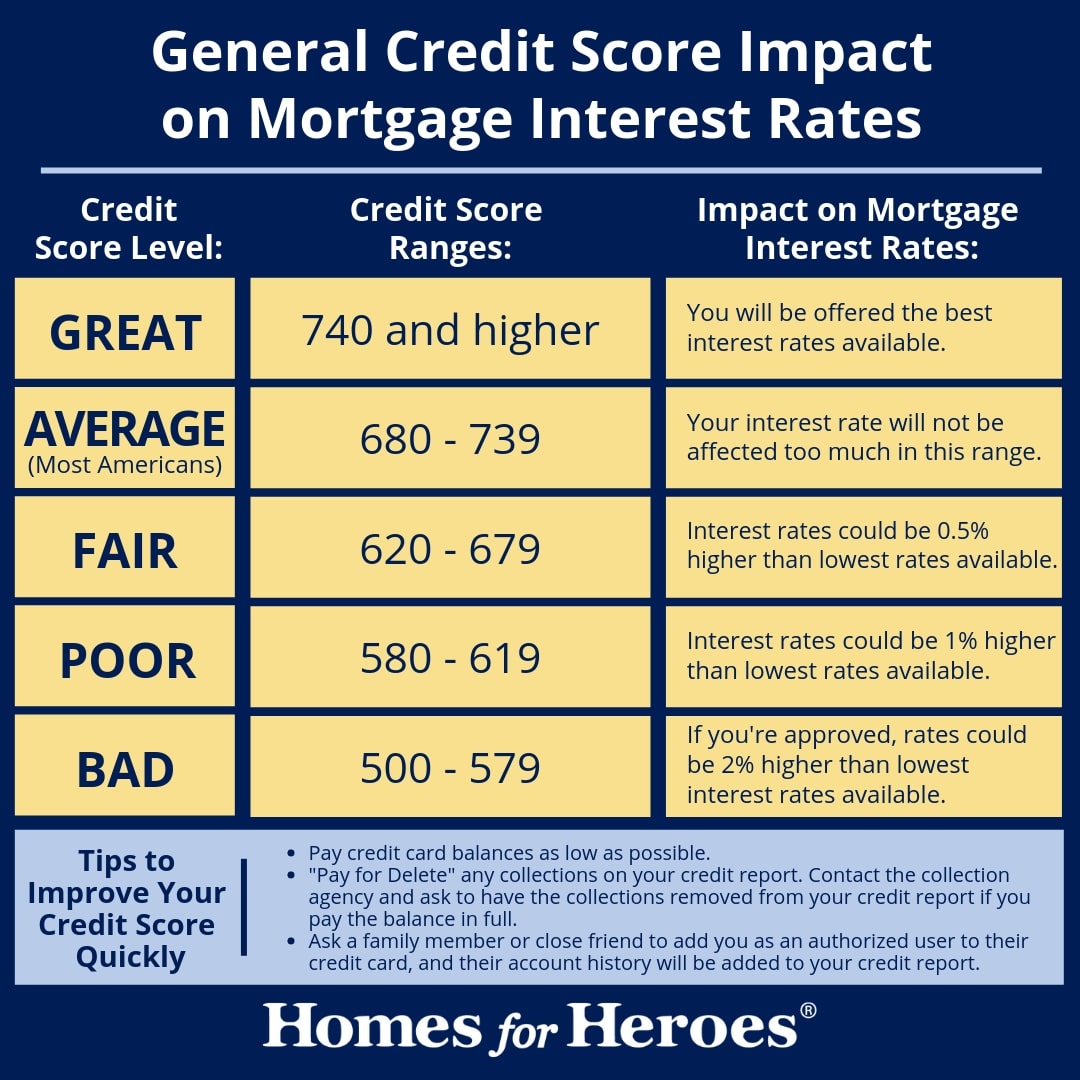

- What is the lowest credit score to buy a house?

- Getting a Mortgage with Bad Credit

If you need to increase the available credit to improve your utilization, applying for new accounts is an option. While this will lead to hard inquiries, they won’t stay on your credit report forever. Newer credit accounts harm the average age, and it also means that a hard inquiry has been made on your credit report.

As with FHA loans, your home must meet specific standards to qualify. And while the VA has no specific credit score minimum, most lenders do. Rocket Mortgage®for example, has a 580 minimum credit requirement. The easiest way to improve your DTI is by shopping for homes at the lower end of your budget.

Minimum Credit Score to Buy a House

The good news is that small changes to your credit can yield significant changes in your score, and with every 20-point improvement, you save money. Having bad credit doesn’t mean you can’t enjoy the benefits of homeownership. Instead, it might just require additional research when looking for financing. The amount of credit you are currently using is also known as your credit utilization and is responsible for 30% of your score. The more credit you’re using, the higher your credit utilization, the lower your score can become. It would help if you looked to keep your total credit usage under 30%.

Ted Thomas is America’s Leading Authority on Tax Lien Certificates and Tax Deed Auctions, as well as a publisher and author of more than 30 books. His guidebooks on Real Estate have sold in four corners of the world. He has been teaching people just like you for over 30 years how to buy houses in good neighborhoods for pennies on the dollar. He teaches how to create wealth with minimum risk and easy-to-learn methods. Your recent and current economic situation, as well as what happened in the past, gives the lender a good idea of your ability to repay the loan. Companies displayed may pay us to be Authorized or when you click a link, call a number or fill a form on our site.

How much more will it cost to buy a house with bad credit?

As long as you pay your credit card in full, you won't be charged interest. You could literally use it for one $10 purchase per month, pay your $10 credit card bill, and build credit. According to Ramsey, a credit score is really an "I love debt" score. He's against credit scores because he believes they're tied to being in debt. To make his point, he shares misleading information about what goes into a credit score, with the names of the scoring criteria conveniently changed. Not having a credit score is inconvenient, can cost you money, and makes it harder to buy or rent a home.

If you’re considering a hard money lender to finance your house purchase, a payment of 50% down might even be a requirement. However, you should proceed with extreme caution in this scenario. Hard money loans often feature escalated repayment terms, high interest rates, and other terms that make them more expensive and harder to repay. In this guide, we’ll take a deeper look at what buying a house with bad credit looks like and how much it might cost you. We’ll also show you some practical ways to improve your credit score quickly so you can put yourself into a better position as a borrower.

Thinking about buying but not sure where to begin? Start with our affordability calculator.

Low credit scores mean you’re a higher risk for a lender but do not have to mean your dream of owning a home has to come to an end. We spoke to Evelyne Jamet at Vitek Mortgage about the differences among FICO scores and how that relates to the interest rate borrowers are charged. This scenario assumes the borrower with bad credit is putting down 10% of the purchase price in cash.

Foreclosure and bankruptcy do have a long-term impact on your credit, but this doesn't last forever. Bankruptcy stays on your credit report for seven to 10 years, depending on the type of bankruptcy. When you’re buying a home, there’s no such thing as “good credit” or “bad credit” – there is only qualifying credit. After the Great Recession of 2009, subscription-based credit companies emerged to help consumers build good credit. One credit builder, StellarFi, will automatically pay your bills to build your credit.

Mortgage Rates by State

Credit scoring models may reward you for having a healthy mixture of account types on your credit report. With FICO Scores, for example, your credit mix makes up 10% of your credit score. Credit scoring models may still count paid collections against you. Lenders use older versions of the FICO Score when you apply for a mortgage. With older FICO Scores, the presence of the collection account on your report is what hurts your credit score, not the account balance. If you have a loved one with a good credit card account, a simple favor has the potential to improve your credit score.

He can handwave away all the difficulties about not having a credit score, because he has enough money to where it doesn't affect him. For the everyday listener without a net worth in the hundreds of millions of dollars, not having a credit score is a huge, and unnecessary, disadvantage. His advice on credit scores is one of the most problematic examples.

In that case, you might overcome a lender’s reluctance to issue you a loan with bad credit. From a lender’s point of view, chipping in with a large down payment makes you more likely to pay back the mortgage. However, if supplying such a large down payment is within your reach, it might help your case. As mentioned, a significant down payment may make lenders feel more comfortable issuing you a mortgage when you have credit issues.

You can speak with a mortgage broker to get an idea of what to expect from certain lenders before submitting a mortgage application. Is a writer for Clever Girl Finance and co-founder of DollarSanity. She is a part-time digital nomad with a passion for helping people find security and freedom via financial literacy. Note that the payment-for-deletion approach tends to be a long shot. If you find a debt collector that’s willing to agree to such an arrangement, be sure to get the offer in writing before you pay. The rule of thumb is to keep your credit utilization at less than 30%, meaning your total balances shouldn’t exceed 30% of your available credit.

Once your bank account hits your goal down-payment number, keep saving so you have a buffer. Your emergency fund will prepare you for unexpected expenses and life circumstances. If you're buying a $150,000 home and putting down 20% ($30,000), your mortgage loan amount will be $120,000.